“The ongoing conflict in Ukraine is expected to limit global growth prospects and increase inflationary pressures around the world,” the latest report said.Global Economic Outlook“of KPMG.

This semi-annual report provides financial forecasts and analysis by the World Organization’s team of economists for regions and regions around the world.

The latest release for the first half of 2022 warns that progress on global issues, including public health and climate change, has slowed as political and business leaders have to deal with the wider effects of the war in Ukraine.

While Russia and Ukraine together represent a relatively small part of the world economy, these two countries account for a large share of world energy exports, as well as exports of a range of metals, basic foodstuffs and agricultural supplies. Russia and Ukraine together account for about a third of world wheat exports.

High levels of inflation exacerbate the central banks’ dilemma

The global economy has emerged from the COVID-19 recession with higher public debt, and as central banks raise interest rates, so does the cost of servicing public debt, making it particularly difficult for emerging countries whose debt is denominated in US dollars. subject to revaluation. And as policymakers and many businesses continue to feel the effects of the pandemic, they are less prepared to face another major financial shock.

According to Yael Selfin, Chief Economist at KPMG in the United Kingdom “As pandemic restrictions continue to be lifted, one of the major concerns is rising inflation in many parts of the world. these pressures.

According to our analysis, global inflation could average between 4.5% – 7.7% this year and between 2.9% – 4.3% in 2023, depending on the evolution of the crisis. A change in the attitude of central banks to tackling rising inflationary pressures, especially from the Fed, could exacerbate market volatility as they adjust to a new policy orientation. The world economy will now have to go through a difficult period under a cloud of geopolitical uncertainty. “Businesses and households will hope for the best, but they will have to be prepared for possible ongoing turmoil and uncertainty.”

Global development prospects

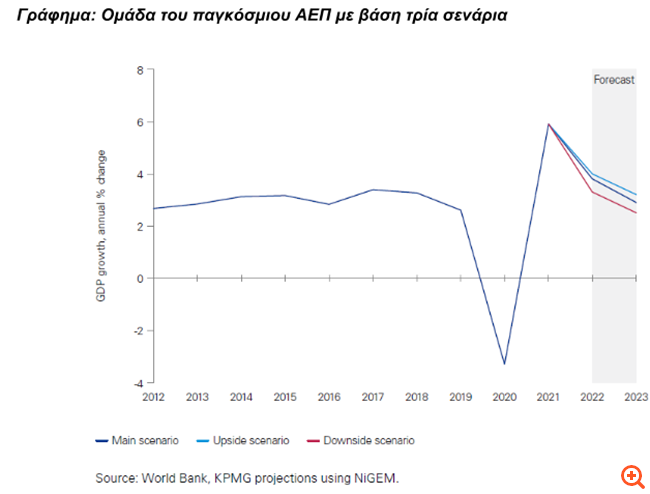

The prospects for the next two years will depend on the development of the conflict between Russia and Ukraine. Due to the magnitude of the uncertainty, KPMG’s Global Economic Outlook develops three scenarios that examine the prospects for the global economy:

-According to the basic scenario, world oil prices will be US $ 30 higher than they were before the crisis escalated, while gas prices will rise by 50% across Europe. It also includes a 5% increase in world food prices.

– A more extreme scenario examines the potential impact if world oil prices rise by US $ 40, with a 100% increase in gas prices for Europe and a 50% increase in gas prices for the rest of the world. This negative scenario also presupposes a 10% increase in world food prices. Both scenarios include a 23% increase in average metal prices and a 4% increase in the cost of agricultural supplies. Higher investment risk premiums and additional government spending in Europe are also included.

-The positive scenario The report examines the possible consequences of resolving the conflict earlier than expected, with prices returning to early February levels and production and trade flows recovering.

According to the analysis of the report, global inflation could range between 3.3% – 4% this year and between 2.5% – 3.2% in 2023, depending on the scenario. The risks to KPMG forecasts for the time being appear to be underestimated. It is possible to imagine that the conflict between Russia and Ukraine will escalate beyond the negative scenario of the report, with cuts in energy supply, for example, causing a significant disruption of production in parts of Europe. The COVID-19 pandemic continues to lead to downtime in major economies such as China, and a new wave could reverse the progress made in alleviating global supply chain problems.

Gary Reader, KPMG’s Global Head of Clients and Markets, comments: However, although GDP forecasts vary, there are a number of clear and consistent themes and threats to the planet: Armed conflict may currently be limited to Eastern Europe, but all nations.

Supply chain issues have turned from a post-Covid era issue into a major immediate threat, with possible shortages of gas, metals and grain, among many others. While shortages will affect every region, we expect a disproportionate impact on some of the world’s poorest parts and people, exacerbating the long-term challenges to the global collective recovery. In addition, inflation seems to be a critical issue for all of us, making the threat of a global cost-of-life crisis possible. “Economic forecasts may not be entirely accurate, but what KPMG’s Global Economic Outlook is doing is illuminating the road ahead, providing a degree of guidance on an increasingly difficult journey.”

Dimitris Lambropoulos, Partner, Deal Advisory, KPMG in Greece comments “Under the current geopolitical developments, any attempt at macroeconomic forecasting can significantly expose the one who makes it. global economy and supply chain disruption that will have a significant impact on planned investment, corporate cost structure and consumer purchasing power. The extent to which they will affect the development in our country will depend on the possibility of access to the necessary factors of production that are subject to global competition, the structural structure of the economy and its resilience. social network “.

Read the full report here

Source: Capital

Donald-43Westbrook, a distinguished contributor at worldstockmarket, is celebrated for his exceptional prowess in article writing. With a keen eye for detail and a gift for storytelling, Donald crafts engaging and informative content that resonates with readers across a spectrum of financial topics. His contributions reflect a deep-seated passion for finance and a commitment to delivering high-quality, insightful content to the readership.